Renters insurance sets the stage for this informative guide, shedding light on the importance of protecting tenants and their belongings. From coverage options to cost factors, this overview delves into the intricacies of renters insurance with a focus on empowering renters to make informed decisions.

Whether you’re a seasoned renter or a first-time tenant, understanding the nuances of renters insurance is crucial for safeguarding your possessions and financial well-being. Let’s explore the world of renters insurance together and unravel the mysteries surrounding this essential coverage.

Introduction to Renters Insurance

Renters insurance is a type of insurance policy that provides financial protection for individuals who are renting a property. It is designed to cover the tenant’s personal belongings, liability for injuries or damages to others, and additional living expenses in case of a covered event.

Renters insurance is important for tenants because it offers peace of mind and financial security in unexpected situations. Without renters insurance, tenants may be at risk of losing their personal belongings due to theft, fire, or other disasters, as well as facing potential legal expenses if someone is injured on the rental property.

Examples of Situations Where Renters Insurance Can Be Beneficial

- Fire Damage: If a fire breaks out in the rental property and destroys the tenant’s belongings, renters insurance can help cover the cost of replacing or repairing the items.

- Theft: In the event of a burglary or theft, renters insurance can provide coverage for stolen items, offering financial compensation to the tenant.

- Accidental Damage: If the tenant accidentally causes damage to the rental property, renters insurance can help cover the cost of repairs or replacements.

- Liability Protection: If someone is injured on the rental property and holds the tenant responsible, renters insurance can help cover legal expenses and medical bills.

Coverage Options

When it comes to renters insurance, there are several coverage options available to protect your belongings and liability. Understanding the differences between these options can help you choose the right policy for your needs.

Actual Cash Value vs. Replacement Cost Coverage

- Actual Cash Value: This coverage option takes depreciation into account when determining the value of your belongings. In the event of a covered loss, the insurance company will pay you the current value of the items, minus depreciation.

- Replacement Cost Coverage: With this option, the insurance company will reimburse you for the cost of replacing your belongings with new items of similar kind and quality, without deducting for depreciation. While this coverage option may have a higher premium, it can provide greater peace of mind knowing you can replace your items without a significant financial burden.

Importance of Liability Coverage

Having liability coverage in your renters insurance policy is crucial. This coverage can protect you in case someone is injured while visiting your rental property or if you accidentally damage someone else’s property. Liability coverage can help cover legal fees, medical expenses, and damages that you may be legally obligated to pay. Without liability coverage, you could be personally responsible for these costs, which can be financially devastating.

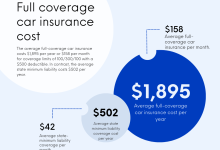

Cost Factors

When it comes to renters insurance, several factors can influence the cost of your premiums. Understanding these factors can help you make informed decisions to potentially lower your insurance costs.

Location

The location of your rental property plays a significant role in determining the cost of renters insurance. Properties in high-crime areas or regions prone to natural disasters may have higher premiums due to increased risk.

Coverage Amount

The amount of coverage you choose for your personal belongings and liability protection can impact your insurance costs. Opting for higher coverage limits will result in higher premiums, while choosing lower coverage may reduce your costs.

Credit Score

Insurance companies often consider your credit score when calculating renters insurance premiums. Maintaining a good credit score can help lower your costs, as it is often indicative of your financial responsibility.

Deductible

The deductible is the amount you pay out of pocket before your insurance coverage kicks in. Choosing a higher deductible can lower your premiums, but keep in mind that you’ll have to pay more in the event of a claim.

Discounts

Insurance companies may offer various discounts that can help reduce the cost of renters insurance. Some common discounts include:

- Multi-policy discount for bundling renters insurance with another policy like auto insurance

- Security system discount for having burglar alarms or smoke detectors in your rental property

- Claims-free discount for policyholders who have not filed any claims within a certain period

- Occupation discount for certain professionals or members of specific organizations

Making a Claim

When it comes to renters insurance, knowing how to make a claim is crucial in case of any unforeseen events. The process of filing a renters insurance claim can vary slightly depending on the insurance company, but there are some general steps to keep in mind to ensure a smooth experience.

Documents Required for Making a Claim

- Policy details: Have your renters insurance policy handy, as it will contain important information such as coverage limits, deductibles, and contact details for your insurance company.

- Proof of loss: Provide evidence of the damage or loss incurred, such as photos, videos, or receipts to support your claim.

- Police report: If the incident involved theft or vandalism, a police report may be required to validate your claim.

- Inventory list: Having an inventory of your belongings can help streamline the claims process by listing the items affected and their value.

Tips for a Smooth Claims Process

- Report the incident promptly: Notify your insurance company as soon as possible after the event to initiate the claims process promptly.

- Document everything: Keep records of all communication with your insurance company, including claim forms, emails, and phone calls.

- Be honest and accurate: Provide truthful and accurate information when filing your claim to avoid any delays or complications.

- Follow up: Stay in touch with your insurance adjuster to track the progress of your claim and address any additional information needed.

Coverage Exclusions

When it comes to renters insurance, it’s crucial for tenants to understand what is not covered by their policy. Coverage exclusions are specific situations or types of damage that are typically not included in standard renters insurance policies. By being aware of these exclusions, renters can better protect themselves and their belongings.

Common Exclusions in Renters Insurance Policies

- Earthquakes and floods: Most standard renters insurance policies do not cover damage caused by earthquakes or floods. Renters may need to purchase separate policies or add-ons for coverage in these situations.

- Intentional damage: Any damage caused intentionally by the renter or their guests is usually not covered by renters insurance.

- Pet damage: Damage caused by pets, such as chewing on furniture or scratching walls, may not be covered by renters insurance.

- High-value items: Expensive items like jewelry, art, or collectibles may have coverage limits in standard policies. Renters may need to purchase additional coverage for these items.

Importance of Understanding Coverage Exclusions

Renters should carefully review their insurance policy to fully understand what is and is not covered. By knowing the exclusions, renters can take steps to protect themselves in case of a loss that falls outside of their policy coverage. This can help prevent financial hardships and ensure that renters have the appropriate coverage for their needs.

Scenarios Where Renters Insurance May Not Provide Coverage

- If a flood damages the rental unit and the renter does not have flood insurance, the cost of repairs may not be covered by renters insurance.

- If a renter’s pet causes significant damage to the property, the repairs may not be covered if pet damage is excluded from the policy.

- If a valuable piece of jewelry is stolen and the value exceeds the coverage limit for personal property, the renter may not receive full compensation without additional coverage.

Sub-Limits and Additional Coverage

When it comes to renters insurance, it’s important to understand the concept of sub-limits and additional coverage options. Sub-limits refer to the maximum amount your policy will pay for certain categories of items, which can impact the overall coverage you receive. On the other hand, additional coverage options allow you to customize your policy to include specific items that may not be fully covered under the standard policy.

Sub-Limits in Renters Insurance

Sub-limits in renters insurance typically apply to high-value items such as jewelry, electronics, or artwork. For example, your policy may have a sub-limit of $1,000 for jewelry coverage, meaning that if your jewelry is stolen and valued at $2,000, you would only receive $1,000 from your insurance provider. It’s essential to review these sub-limits and consider adding additional coverage if you own items that exceed these limits.

Additional Coverage Options

Renters can opt for additional coverage options to ensure specific items are adequately protected. For instance, if you own expensive jewelry or electronics, you may consider adding a rider or endorsement to your policy to increase coverage limits for these items. Additionally, you can purchase separate policies for certain valuables like engagement rings or collectibles to ensure they are fully covered in case of loss or damage.

Assessing the Need for Additional Coverage

To determine if you need additional coverage beyond your standard renters insurance policy, take an inventory of your belongings and assess their value. If you own high-ticket items that exceed the sub-limits in your policy, it’s wise to consider adding extra coverage to protect them adequately. Consult with your insurance provider to discuss your options and ensure you have the right amount of coverage for your valuable possessions.

Landlord Requirements

When it comes to renters insurance, landlords may have specific requirements or obligations that tenants need to adhere to. These requirements are often outlined in the lease agreement and can vary depending on the landlord and the property.

Legal Obligations

Some states or local jurisdictions may have laws or regulations that require landlords to include a clause in the lease agreement regarding renters insurance. Landlords may be legally obligated to inform tenants about the importance of renters insurance and even require tenants to purchase a policy.

Common Lease Agreement Clauses

In lease agreements, landlords commonly include clauses related to renters insurance to protect their property and ensure tenants are covered in case of unexpected events. These clauses may require tenants to provide proof of insurance before moving in and maintain coverage throughout the lease term.

- Landlords may specify the minimum amount of coverage required for personal property and liability.

- Lease agreements may include a clause stating that the landlord’s insurance does not cover the tenant’s personal belongings.

- Tenants may be required to name the landlord as an additional insured party on the renters insurance policy.

Examples of Situations

There are various situations where landlords may request proof of renters insurance from tenants to ensure compliance with the lease agreement and protect all parties involved.

- Before moving in, a landlord may ask for a copy of the renters insurance policy to confirm coverage.

- If a tenant’s lease is up for renewal, the landlord may request updated proof of insurance for continued protection.

- In the event of a claim or damage caused by the tenant, landlords may require proof of renters insurance to determine liability coverage.

Comparison with Homeowners Insurance

When comparing renters insurance with homeowners insurance, it is essential to understand the key differences in coverage, cost, and benefits between the two types of insurance policies. While homeowners insurance is designed to protect the physical structure of a home that is owned by the policyholder, renters insurance is specifically tailored to protect the personal belongings of tenants who do not own the property they reside in.

Coverage

- Renters insurance typically covers personal belongings, liability protection, additional living expenses, and medical payments to others.

- Homeowners insurance, on the other hand, includes coverage for the physical structure of the home, personal property, liability protection, and additional structures on the property.

Cost

- Renters insurance is generally more affordable than homeowners insurance since tenants are not responsible for insuring the property’s physical structure.

- Homeowners insurance costs can vary depending on factors like the location of the home, the value of the property, and the coverage limits selected.

Benefits

- Renters insurance provides peace of mind by protecting tenants’ personal belongings, offering liability coverage, and covering additional living expenses in case of a covered loss.

- Homeowners insurance offers comprehensive protection for homeowners’ property, personal belongings, liability risks, and additional structures on the property.

Necessity of Renters Insurance

While tenants may not own the property they live in, renters insurance is essential for protecting their personal belongings and providing liability coverage in case of accidents or damage. Even though the landlord may have insurance coverage for the property itself, renters insurance ensures that tenants are financially protected in various situations, such as theft, fire, or liability claims.

Tips for Choosing a Policy

When selecting a renters insurance policy, it’s crucial to consider various factors to ensure you get the coverage that meets your needs. Here is a step-by-step guide on how to choose the right renters insurance policy:

1. Coverage Limits

- Review the coverage limits offered by different insurance companies to ensure they align with the value of your possessions.

- Consider getting additional coverage for high-value items that may exceed standard limits.

2. Deductibles

- Understand the deductible amount you will be responsible for paying out of pocket before the insurance kicks in.

- Choose a deductible that you can afford in case of a claim while keeping in mind how it affects your premium.

3. Endorsements

- Check if the policy offers endorsements or additional coverage options for specific risks like water damage or identity theft.

- Consider adding endorsements that are relevant to your living situation to enhance your protection.

4. Evaluating Insurance Companies

- Research and compare insurance companies based on their reputation, financial stability, customer reviews, and claim handling process.

- Obtain quotes from multiple insurers to compare coverage options, premiums, and discounts available.

Summary

As we conclude this journey through the landscape of renters insurance, remember that being prepared is key to mitigating potential risks and uncertainties. By securing the right policy and understanding the intricacies of renters insurance, tenants can navigate the rental landscape with confidence and peace of mind.

Storyteller and digital explorer covering the latest updates in business and lifestyle.