Private health insurance is a crucial aspect of healthcare planning, offering a range of coverage options, cost factors, and benefits that cater to individual needs. This comprehensive guide delves into the intricacies of private health insurance to help you make informed decisions about your healthcare needs.

The Basics of Private Health Insurance

Private health insurance refers to a type of coverage that individuals purchase from a private insurance company to help cover medical expenses. Unlike public health insurance programs like Medicare or Medicaid, private health insurance is typically obtained through an employer or purchased independently.

Examples of Private Health Insurance Companies

- UnitedHealth Group

- Anthem

- Kaiser Permanente

- Cigna

- Humana

Benefits of Having Private Health Insurance

Private health insurance offers several benefits to individuals, including:

- Access to a broader network of healthcare providers

- Shorter wait times for appointments and procedures

- More coverage options for specialized treatments

- Additional services such as dental and vision care

- Ability to choose your own doctor or specialist

Coverage Options

Private health insurance offers a variety of coverage options to cater to different individual needs. These options can vary significantly from public health insurance, providing more personalized and specialized coverage.

Types of Coverage

- Basic Coverage: Includes essential services such as hospital stays, doctor visits, and prescription drugs.

- Comprehensive Coverage: Offers a wider range of services, including specialist consultations, mental health treatment, and alternative therapies.

- Add-Ons: Additional coverage options that can be purchased to enhance your policy, such as dental, vision, or maternity care.

Comparison with Public Health Insurance

- Public health insurance typically offers basic coverage for essential services, while private insurance provides more extensive coverage options.

- Private insurance allows for more flexibility in choosing healthcare providers and accessing specialized treatments not covered by public insurance.

- Public insurance is funded by taxpayers and has eligibility requirements, while private insurance is paid for by individuals or employers.

Individualized Coverage

Private health insurance allows individuals to tailor their coverage based on their specific needs and preferences. This customization can include selecting deductibles, coverage limits, and network providers that align with personal healthcare requirements. By offering a range of coverage options, private health insurance ensures that individuals can access the care they need in a way that suits their unique circumstances.

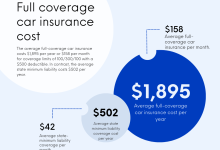

Cost Factors

Private health insurance costs can vary based on several key factors that influence the overall pricing of coverage. Understanding these factors is essential for managing the cost of private health insurance effectively.

Factors Influencing Cost

- Age: Younger individuals typically pay lower premiums compared to older individuals due to a lower risk of health issues.

- Health History: Pre-existing conditions or a history of medical issues can increase the cost of insurance.

- Location: The cost of healthcare services and insurance can vary based on where you live.

- Coverage Level: The extent of coverage and benefits included in the plan will affect the cost.

Deductibles and Premiums

Deductibles and premiums are important components of private health insurance that impact the overall cost of coverage. Deductibles are the amount you must pay out of pocket before your insurance starts covering costs, while premiums are the monthly payments you make to maintain coverage.

- Higher deductibles usually result in lower monthly premiums, but you will have to pay more out of pocket before insurance kicks in.

- Lower deductibles mean higher monthly premiums, but you will have to pay less out of pocket when seeking medical care.

- Choosing the right balance between deductibles and premiums can help you manage costs based on your healthcare needs and budget.

Managing Costs

- Compare Plans: Shop around and compare different private health insurance plans to find one that offers the best value for your needs.

- Consider Subsidies: Check if you qualify for any government subsidies or tax credits that can help lower the cost of insurance.

- Utilize Preventive Care: Regular check-ups and preventive services can help you avoid costly medical treatments in the future.

- Review Your Coverage: Periodically review your coverage to ensure you are not paying for services you do not need.

Network Providers

When it comes to private health insurance, network providers play a crucial role in determining the cost and coverage of your healthcare services. Network providers are healthcare professionals, facilities, and hospitals that have agreed to provide services at a discounted rate to members of a specific insurance plan.

Advantages and Disadvantages of Network Providers

- Advantages of using in-network providers:

- Lower out-of-pocket costs: Insurance plans typically cover a higher percentage of the costs when you visit an in-network provider.

- Predictable costs: Since in-network providers have pre-negotiated rates with the insurance company, you are less likely to receive unexpected bills.

- Coordinated care: In-network providers often work together to ensure you receive comprehensive and coordinated care.

- Disadvantages of using out-of-network providers:

- Higher costs: Out-of-network providers may charge higher rates, leading to higher out-of-pocket expenses for you.

- Limited coverage: Insurance plans may offer limited or no coverage for out-of-network services, leaving you responsible for a larger portion of the bill.

- Reimbursement delays: You may have to pay the full cost upfront when seeing an out-of-network provider and then wait for reimbursement from your insurance company.

Tips for Finding Network Providers

- Check your insurance provider’s website: Most insurance companies have online directories where you can search for in-network providers based on your location and healthcare needs.

- Ask for recommendations: Your primary care physician or friends and family members may be able to recommend network providers that they have had positive experiences with.

- Verify coverage: Before scheduling an appointment, confirm with the provider’s office that they are still part of your insurance network to avoid any surprise bills.

- Consider telehealth options: Some insurance plans offer virtual visits with network providers, which can be a convenient and cost-effective way to receive care.

Enrollment Process

When enrolling in a private health insurance plan, there are several important steps to follow to ensure you get the coverage you need. Below is a checklist for individuals considering private health insurance for the first time, as well as information on enrollment periods and deadlines.

Checklist for Enrollment

- Evaluate your healthcare needs and budget to determine the type of coverage you require.

- Research different private health insurance plans available in your area to compare benefits and costs.

- Contact insurance providers directly or use a broker to get quotes and more information.

- Fill out the enrollment application accurately and provide any necessary documentation.

- Pay the premium for your chosen plan to activate coverage.

Enrollment Periods and Deadlines

Private health insurance plans have specific enrollment periods during which you can sign up for coverage. It is important to be aware of these deadlines to avoid gaps in coverage.

It is crucial to enroll during the open enrollment period to avoid penalties or restrictions on getting coverage outside of this period.

- Open Enrollment Period: This is the designated time each year when individuals can enroll in or make changes to their health insurance plans.

- Special Enrollment Period: Qualifying life events, such as getting married, having a baby, or losing other coverage, may trigger a special enrollment period outside of the annual open enrollment period.

- Initial Enrollment Period: When you first become eligible for private health insurance, you have a window of time to enroll without facing penalties.

Claims and Reimbursements

When it comes to private health insurance, understanding the process of filing claims and maximizing reimbursements is crucial for getting the most out of your coverage.

Filing Claims with Private Health Insurance Companies

Filing a claim with your private health insurance company typically involves submitting relevant documentation, such as medical bills and receipts, to your insurer. This can usually be done online through the insurer’s portal or by mailing in the necessary paperwork.

Common Reasons for Claim Denials and How to Avoid Them

- Incorrect information: Ensure all details on your claim form are accurate and up to date to avoid any potential denials.

- Out-of-network providers: Make sure to visit healthcare providers within your insurance network to prevent claim denials due to out-of-network services.

- Pre-authorization requirements: Familiarize yourself with any pre-authorization requirements for certain medical procedures or treatments to avoid claim denials.

Tips for Maximizing Reimbursements from Private Health Insurance Plans

- Keep thorough records: Maintain detailed records of all medical expenses and treatments to ensure accurate reimbursement.

- Understand your coverage: Familiarize yourself with your insurance plan to know what services are covered and how to maximize reimbursements for eligible expenses.

- Submit claims promptly: File your claims in a timely manner to avoid any potential delays or issues with reimbursements.

Additional Benefits

Private health insurance plans offer a range of additional benefits beyond basic coverage. These lesser-known perks can enhance your overall healthcare experience and help you stay healthy. Let’s explore some of the unique benefits that private health insurance companies may offer:

Wellness Programs

Wellness programs are designed to promote healthy behaviors and prevent illness. These programs may include fitness incentives, smoking cessation support, nutrition counseling, and stress management resources. By participating in wellness programs, policyholders can proactively improve their health and well-being.

Telemedicine Services

Telemedicine services allow policyholders to consult with healthcare providers remotely, using video calls or online messaging. This can be especially convenient for minor health concerns, follow-up appointments, or when access to in-person care is limited. Telemedicine services can save time and provide quick medical advice from the comfort of home.

Preventive Care Coverage

Many private health insurance plans cover preventive care services at no additional cost to the policyholder. This can include vaccinations, screenings, annual check-ups, and preventive medications. By prioritizing preventive care, policyholders can detect and address potential health issues early, leading to better health outcomes and reduced healthcare costs in the long run.

Examples of Unique Benefits

Some private health insurance companies offer innovative benefits such as gym membership discounts, mental health resources, alternative therapies coverage, and personalized wellness coaching. These unique benefits cater to diverse healthcare needs and preferences, providing a comprehensive approach to healthcare beyond traditional medical services.

Renewal and Changes

When it comes to private health insurance, renewal and changes are important aspects to consider to ensure you have the coverage you need. Whether you are renewing your current plan or making adjustments to better suit your needs, it’s essential to understand the process and factors involved.

Factors to Consider for Renewal

- Review your current coverage: Take the time to assess whether your current plan still meets your healthcare needs. Consider any changes in your health status or lifestyle that may require different coverage.

- Premium costs: Evaluate any changes in premium costs for the upcoming renewal period. Compare these costs with the benefits and coverage provided by your plan.

- Network providers: Check if your preferred healthcare providers are still part of the network covered by your plan. Ensure that you have access to quality care when needed.

- Add-on options: Assess any add-on options or additional benefits offered by your insurance provider. Determine if there are new options that may be beneficial for you.

Making Changes to Your Plan

- Adding dependents: If you need to add dependents to your plan, such as a spouse or children, contact your insurance provider to understand the process and any additional costs involved.

- Adjusting coverage: If you wish to adjust your coverage levels, such as increasing or decreasing certain benefits, discuss these changes with your insurer to ensure you have the right level of coverage for your needs.

- Policy upgrades: If you are considering upgrading your policy to a higher tier with more comprehensive coverage, review the options available and the impact on your premium.

Timeline for Reviewing and Updating

- Annual review: It is recommended to review your private health insurance policy annually to ensure it aligns with your current healthcare needs and financial situation.

- Open enrollment period: Take advantage of the open enrollment period to make any changes to your plan without penalties. This period typically occurs once a year.

- Life events: In case of major life events such as marriage, childbirth, or change in employment, consider reviewing and updating your health insurance coverage to reflect these changes.

Customer Support

Customer support plays a crucial role in the overall experience of having private health insurance. It is essential for policyholders to have access to reliable and efficient customer service for various inquiries, assistance, and issue resolution.

Importance of Customer Support

Good customer support offered by private health insurance companies can greatly enhance the overall experience for policyholders. It ensures that individuals have access to assistance when navigating their coverage options, understanding their benefits, submitting claims, and resolving any issues that may arise. Prompt and helpful customer support can increase customer satisfaction and trust in their insurance provider.

- Customer support assists policyholders in understanding their coverage options and benefits, ensuring they make informed decisions regarding their healthcare.

- It provides guidance on the enrollment process, helping individuals navigate the complexities of choosing a plan that suits their needs.

- Efficient customer support can help expedite the claims and reimbursement process, minimizing delays and frustrations for policyholders.

- In cases of disputes or issues with coverage, customer support can work towards resolving conflicts and ensuring policyholders receive the benefits they are entitled to.

Enhancing the Overall Experience

Effective customer support can enhance the overall experience of having private health insurance by providing timely assistance, clear communication, and personalized support to policyholders. It fosters a sense of trust and confidence in the insurance provider, leading to higher satisfaction levels among customers.

- Timely responses to inquiries and issues can help alleviate concerns and provide peace of mind to policyholders.

- Clear and concise communication from customer support representatives can help policyholders better understand their coverage and benefits.

- Personalized support tailored to individual needs can make policyholders feel valued and supported throughout their healthcare journey.

- Resolving issues efficiently and effectively demonstrates the insurance provider’s commitment to customer satisfaction and quality service.

Future Trends

The landscape of private health insurance is constantly evolving, driven by advancements in technology, changes in regulations, and shifts in consumer preferences. As we look towards the future, several trends are expected to shape the private health insurance industry.

Technological Innovations

Emerging technologies such as artificial intelligence, telemedicine, wearable devices, and data analytics are poised to revolutionize the private health insurance sector. These innovations have the potential to improve efficiency, personalize healthcare services, and enhance the overall patient experience.

- Artificial Intelligence (AI) and Machine Learning: AI-powered tools can help insurers streamline claims processing, detect fraud, and personalize insurance plans based on individual health data.

- Telemedicine: Virtual consultations and remote monitoring services are becoming more prevalent, allowing insurers to offer convenient and cost-effective healthcare solutions to policyholders.

- Wearable Devices: The integration of wearable devices like fitness trackers and smartwatches can enable insurers to promote preventive care and incentivize healthy lifestyle choices among policyholders.

- Data Analytics: Advanced data analytics tools can help insurers assess risk more accurately, identify trends in healthcare utilization, and develop targeted interventions to improve health outcomes.

Regulatory Changes

The private health insurance industry is subject to regulatory oversight, with policies and regulations frequently being updated to address emerging challenges and protect consumer interests. Potential changes in regulations or policies may include:

- Expansion of Coverage Mandates: Governments may introduce new requirements for insurers to cover essential health benefits, preventive services, or emerging medical treatments.

- Consumer Protection Measures: Regulations could be implemented to enhance transparency, affordability, and access to healthcare services for policyholders.

- Digital Health Regulations: With the growing popularity of digital health solutions, regulators may establish guidelines for the use of telemedicine, health apps, and other digital tools within the insurance industry.

Market Disruption

The private health insurance landscape is also susceptible to market disruptions caused by economic fluctuations, demographic changes, and unexpected events such as pandemics or natural disasters. Insurers must remain agile and adaptable to navigate these uncertainties and provide reliable coverage to policyholders.

Outcome Summary

In conclusion, private health insurance plays a vital role in ensuring access to quality healthcare. By understanding coverage options, managing costs effectively, and maximizing benefits, individuals can navigate the complexities of private health insurance with confidence and ease.

Storyteller and digital explorer covering the latest updates in business and lifestyle.